American Farriers Journal

American Farriers Journal is the “hands-on” magazine for professional farriers, equine veterinarians and horse care product and service buyers.

Shane Westman

As much as farriery is art and science, it’s also a business. No matter where you are in your career, you need a plan.

“It’s really important at the beginning of your career, at the mid-stage of your career and toward the twilight of your career to always have a plan,” Bow, Wash., farrier Shane Westman told attendees of the American Association of Professional Farriers (AAPF) Hoofcare Essentials Clinic at Life Data Labs in Cherokee, Ala. “A business plan is a road map for your business life. It helps guide you in making your decisions.”

Your plan should plot where you want to be at various milestones of your career — 5 years, 10 years, 15 years, etc.

“When I started out as a farrier, I had some business experience, mostly in the retail industry,” says the AAPF board member. “I knew that after a year, I wanted to make $100 a day. That was my goal. In 3 years, I wanted to be set with my clientele. In 5 years, I wanted to close my book. In 10 years, I wanted to hire employees. In 20 years, I wanted to have a multi-farrier practice.”

Westman has been shoeing for about 23 years and hasn’t attained all of his goals. That’s OK, he says, changing plans are part of the business.

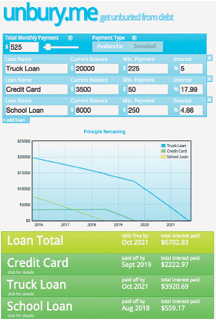

Unbury.me helps you determine which method to use to eliminate your debt.

“I’m still a solo practice,” he says. “I’m not shoeing high-profile horses, although I hope…

American Farriers Journal is the “hands-on” magazine for professional farriers, equine veterinarians and horse care product and service buyers.

American Farriers Journal is the “hands-on” magazine for professional farriers, equine veterinarians and horse care product and service buyers.

Download these helpful knowledge building tools

We are here to support you.

We stock a wide range of high-quality products from trusted brands to ensure durability, performance, and reliability in every job you undertake. Our extensive inventory of horseshoe products and farrier tools means you can find everything you need in one place, saving you time and effort. Your satisfaction is our top priority. We are committed to providing excellent customer service, prompt shipping, and hassle-free returns.