Takeaways

- Analyzing costs and weighing them against profits can help farriers better understand their current financial situation. This can lead to better spending habits and help prioritize setting aside money for the future.

- Protecting yourself and your business from liability concerns through insurance is crucial. It’s also important to have an emergency fund ready for unexpected expenses.

- Avoid debt at all costs, as it’s a barrier to building equity. Part of being financially successful is being free to make purchasing, investment and savings decisions without the added weight of debt.

Day-to-day challenges can make it difficult to sit down and plan for the cost of life’s uncertainties. Though, unexpected expenses such as medical bills or truck repairs don’t have to be financially devastating if properly anticipated. Having business insurance, investing in stocks and retirement accounts, as well as making smart purchases, all pay dividends down the road. Setting yourself and your business up for financial success doesn’t just mean charging more year over year. It also means safeguarding against life’s contingencies and planning for its certainties — like retirement — so that you can feel secure knowing you have your own back.

“Our businesses should be about profit. Yes, we do it for the horse, but we have to feed our families,” says Pennsylvania farrier and certified master financial coach Joshua Sanders at the 2025 International Hoof-Care Summit.

Profitability isn’t solely determined by the amount of cash farriers pocket at the end of the day, but it’s a good measure of immediate stability. For example, a week’s worth of horses should pay for a week’s worth of expenses with extra left over to save, invest or spend. Because of that, it’s crucial to keep cash flowing — one of Sanders’ goals.

When determining how much to raise rates each year, it can be helpful to explore your expenses vs. profit.

“Do we actually make what we think we do?” he asks. “Thirty percent of my profit goes to taxes, and 30% goes toward expenses. If you charge $200, 60% of it — $120 — is gone. I met a farrier who was charging under $100 to shoe a horse. He was a nice guy, and I told him, ‘You may as well work at Walmart because they’re paying $15 per hour. That’s about what you’re making if you’re operating your business correctly.’ ”

Knowing your margin of profit over expenses can also help budget for neglected costs such as insurance, rig replacement and retirement.

Invest in Your Future

Sanders points out that the world today is incredibly litigious. Farriers are at risk of getting sued for events that aren’t in their control, such as a horse being injured while in cross ties. These situations are unpredictable, and liability insurance takes the fear out of that unpredictability. Sanders’ personal liability insurance typically prevents him from grabbing horses out of stalls. While it may feel overly restrictive, it’s an important step in protecting your finances should anything happen.

Another way to help protect yourself is to file as an LLC or an S-Corporation. Without that designation, Sanders says farriers are exposed to additional liability.

“Yes, we do it for the horse, but we have to feed our families…”

“Without it, there’s no entity protecting your personal money, so someone can go after you directly if they decide to sue you. The amount of money it costs to become an LLC or S-Corp is minuscule for the peace of mind it gives you,” he says.

When it comes to auto insurance, Sanders advocates that any truck driven for work should be protected under a commercial policy rather than a personal one. After an accident, regardless of fault, many personal insurance policies won’t cover the cost if they learn it was a work vehicle, he says.

Should a farrier die by a car accident, horse or other unfortunate event, Sanders recommends term life insurance, which he says is saving him money compared with full life insurance. Additionally, once he retires, he no longer sees the need for life insurance, with his own savings and investments then covering his family’s needs should he pass away. For a 30-year life insurance term, his desired payout is 10 times his take home-pay per year.

“I always tell people I’m worth more dead than alive,” he says. “If I die, my wife’s set, so I don’t have to worry about it. It’s a lot of peace of mind.”

Barring any unfortunate events, Sanders plans to retire before he’s 60.

“From previous injuries, I know my body won’t make it until my 70s or 80s,” he says. “So, think about when you want to retire. Set a goal and put it up on your fridge. Say, ‘this is how much I’m investing every month.’ ”

Little Ways to Save

Tightly managing any expenses and avoiding debt are good ways to build equity. However, it can be quickly and unknowingly hampered by rogue spending. One of Sanders’ ways to save is simply by cutting out gas station or fast food impulse buys.

“The average cost of a Starbucks coffee is $4.50. Over 30 days, that’s $135. If you invest that money over 30 years at a 10% return, that’s $305,000 just by cutting out your daily cup of coffee. We don’t have to retire broke,” he says.

On the road, another way to compound your savings is to find deals or enter rewards programs for frequent purchases like gasoline. Sanders averages $100 per month in savings on gas because of this enterprising mindset. This $1,200 per year bump can significantly improve retirement savings.

For big purchases, Sanders has a rule to delay buying an item until he can sleep on it. It mitigates impulse spending by helping him evaluate whether an item would truly be useful or if it would just be convenient. At the International Hoof-Care Summit Trade Show, Sanders made a big purchase for his business but not before waiting a day first.

“My rule of thumb is if it’s over $200, I don’t purchase it for 24 hours. If it’s over $1,000, I wait a week,” he says.

Sanders recommends setting aside 15% of your income for retirement after taxes. For example, if a farrier made $100,000 and taxes took out 30%, invest 15% of the remaining $70,000 before other expenses. Calculating this amount at the beginning of the year can help farriers set aside money each month rather than at the end of the year or sporadically. To save additional money for retirement, investment accounts are also a good option.

“If you invest in a good growth stock mutual fund at $1,200 per month — which can be done if you’re out of debt and making money as a farrier — you’ll be over $2 million in savings after 30 years at a 10% return. The next step is to save for your children’s college fund,” he advises.

Safeguard Against Debt

Injuries, truck breakdowns or other emergencies are events no one likes to think about but are crucial to plan for. Insurance and retirement planning are long-term investments in peace of mind, and setting aside money for emergencies is an investment in debt management.

“When you first start your business, you must have $3,000 to $5,000 in savings for emergency expenses,” Sanders says. “That will cover multiple tool failures. If your trailer door breaks or your forge dies on you, you have savings for emergency business expenses at all times in a separate business account that you don’t touch.”

For personal finances, which should be separate from business, Sanders recommends saving 6 months’ worth of expenses in an emergency fund. It’s the amount of time a farrier could be out of work after a surgery, he says, and it’s also roughly the amount of time it takes until long-term disability insurance payments begin. These cover around 60% of take-home pay. Especially if a farrier is the main breadwinner for their family, Sanders recommends purchasing disability insurance for its security.

“Have $3,000 to $5,000 in savings for emergency expenses…”

These nest eggs can help farriers avoid going into debt because of an emergency, something Sanders strongly advises against. Though the initial costs of starting a business can feel immense, he cites a budget of $10,000, a figure he recommends having in liquid assets.

“For me, there is not a single reason I will say yes to debt other than a mortgage,” he says.

Daily and monthly expenses eat into a savings account quickly, especially with loans to pay off, one of the most common being a car loan. Across the country, the average new car payment is about $750 per month. For people who abuse their cars, Sanders says, the risk of accumulating negative equity — the car being worth less than the remainder of the loan — is not worth it.

He cites Proverbs 22:7 when discussing debt: “The rich rule over the poor, and the borrower is a slave to the lender.”

“I view debt as a prison,” he says. “Your best wealth-building tool is your income. So, if you’re spending it on an auto loan, you’re not using your income to its full potential. Debt limits your ability to build wealth. If we’re running our business correctly, we can make a fantastic living, but there are too many farriers who have to work at 70 or 80 years old.”

Managing Debt While Giving Back

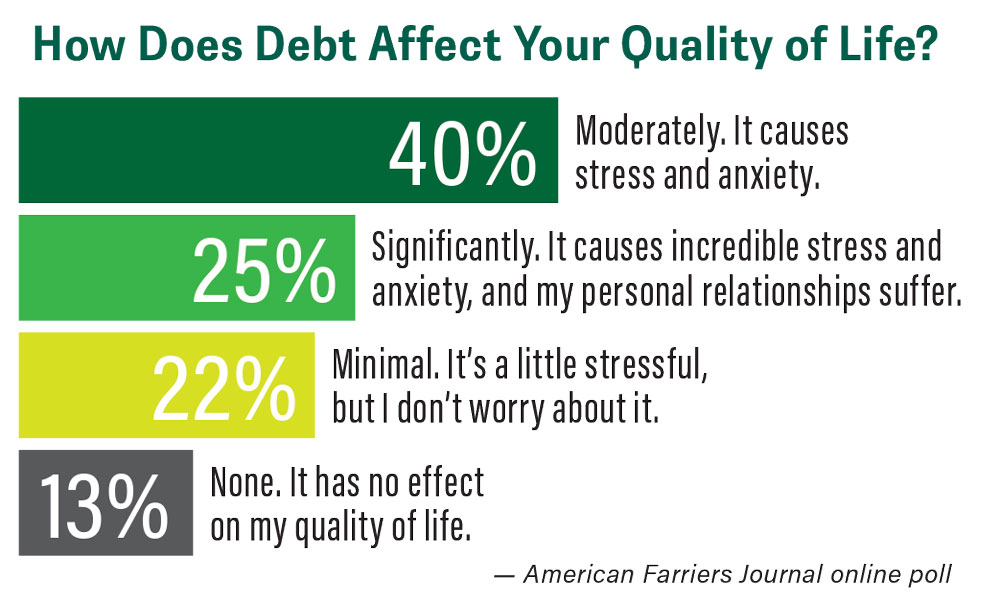

An American Farriers Journal poll found that most farriers with debt feel moderately or significantly stressed about it, to the point it affects their well-being and/or personal relationships. Once the debt is created, no matter how big or small, it’s difficult to get rid of. For Pennsylvania farrier Joshua Sanders, eliminating this debt is priority number one outside of regular or emergency expenses.

“If you are in debt other than your mortgage, the first thing to do is save a $1,000 emergency fund. If you have $10,000 at the bank, you wipe it down to $1,000 and pay off your debt as much as you can with that other money,” he advises.

The next step is to list all debts from smallest to largest and pay off this debt snowball in that order. Once that is complete, then he recommends restarting a 3-6-month emergency fund and retirement contributions. This plan may not work for everyone depending on their other expenses, family needs, age or other circumstances. However, as a general rule, less debt equals less stress.

No debt also frees up finances to give back to your community. Sanders follows the biblical guideline of a 10% tithe. For others, this can be donating to a charity or a cause of personal importance.

However, debt does not have to supersede a charitable donation. The donation can also be 10% of your time each month, whether volunteering, being a mentor to others or offering up other resources. For Sanders, the important part is to give from the heart — while still being smart about your money.

It’s also important to consider tax write-offs when determining whether a new business purchase is worth the money. Write-offs are not a dollar for dollar exchange, Sanders says, and should not be thought of as a 100% reimbursed expense at the end of the year.

“If I spend an extra $100 at the end of the year, I’m not going to get $100 in tax credit for that. Depending on the expense, you get around $0.30 on the dollar in tax credit. Big purchases at the end of the year do not always make sense unless you’re trying to go down a tax bracket, which would allow you to pay a smaller percentage in taxes,” he says.

When it’s necessary, as with a mortgage, he says the monthly payment should not be more than 25% of your take-home pay before health insurance. Using debt to maintain a lifestyle is unsustainable, he warns, and should be taken on only in rare or unavoidable circumstances.

Having money set aside for unexpected expenses and planning early for retirement can help farriers stay out of debt in the long run. While insurance can feel like investing heavily into a “maybe,” the peace of mind it brings is worth it, Sanders says. Financial success isn’t just about being capable of buying big-ticket items; it’s also about securing your future against all possibilities.