Farrier Takeaways

- An IRA is the easiest way to start saving for retirement.

- One-participant 401(k) plans offer flexibility when business fluctuates.

- Some plans allow catch-up contributions.

As a self-employed farrier, enrolling in an employer-sponsored retirement plan isn’t an option. You’re on your own and you want to get serious about saving for retirement by opening a dedicated account, but where do you start? How do you maximize your investment? Is there something better than a standard savings account that offers minimal interest payments? And if you get a late start on retirement savings, can you make up ground somehow?

Not to worry. IRS regulations offer several retirement plan options for the self-employed. And establishing such an account isn’t difficult.

Making Plans

In each of the plans, your contributions are placed into investments such as stocks, bonds, mutual funds or money market accounts in the hope that returns will outpace the interest rates paid on simple savings and checking accounts. You choose the level of risk to your investments (losses are possible) vs. the potential growth of your account.

Brian Kaminski, a financial advisor since 1987 and owner and president of Select Advisor Group Inc., based in Brookfield, Wis., offers insights that can help you choose the right plan.

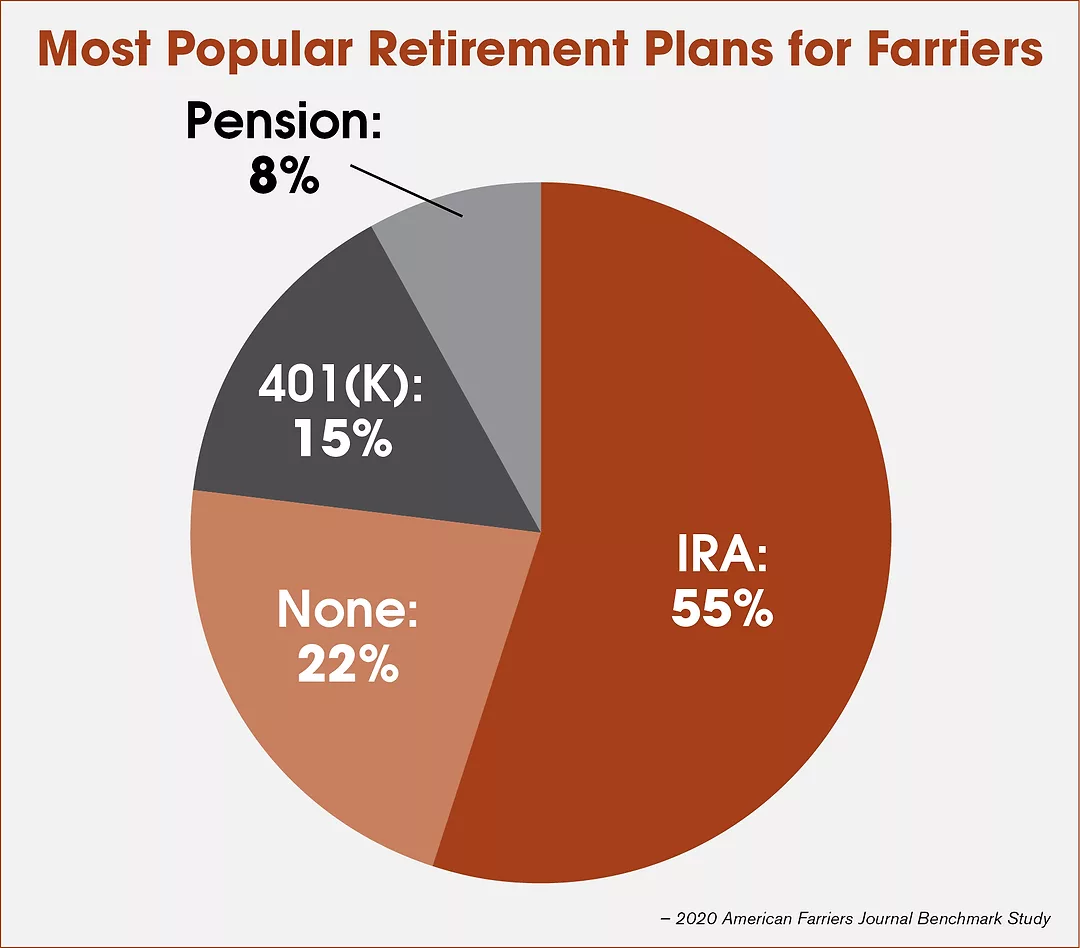

Traditional or Roth IRA. An Individual Retirement Account (IRA) permits you to invest money each year and the contributions are not counted toward your annual taxed income. The contributions and earnings are tax-deferred until withdrawals begin at age 59½ or later. In a Roth IRA, the money contributed is included in taxable gross income in the year of the contribution, but later distributions from the account, including earnings, are tax-free.

IRAs are open to anyone with earned income, although Roth IRAs have income limits. An IRA also can be used in combination with other plans, but the amount of traditional IRA contributions you can deduct from your income taxes might be reduced. If you’re leaving a job to start your own farrier business, you can roll your old 401(k) into an IRA.

The limit on IRA contributions is $6,000 in 2021, plus a $1,000 catch-up contribution for those 50 or older. Financial penalties are incurred for early withdrawals from any IRA account, although there are allowable exceptions.

Kaminski notes that Roth IRA rules are more flexible for those 59 and younger.

“You can withdraw contributions you made to your Roth IRA anytime, tax and penalty free,” he says. “However, you may have to pay taxes and penalties on the earnings in your Roth IRA that you’ve had less than 5 years.”

Kaminski believes an IRA can be a good fit for many farriers.

“It’s probably the easiest way for self-employed people to start saving for retirement,” he says. “You simply open an IRA at an online brokerage and report contributions on your tax return each year. There are no special filing requirements, and you can use it even if you have employees.”

One-participant 401(k) plan. A one-participant 401(k) plan is also known as a solo 401(k), individual 401(k) or uni-401(k). It is largely the same as 401(k) plans offered by larger employers, except that it prohibits other employees beyond your spouse from working for the business. You make contributions pre-tax and distributions after 59 ½ years of age are taxed.

This plan, Kaminski says, “is particularly attractive for those who can and want to save a great deal of money for retirement or those who want to save a lot in some years — say, when business is flush — and less in others. It’s easy to set up, although you’ll need to file paperwork with the IRS each year once you have more than $250,000 in your account.”

A solo 401(k) plan allows for annual salary deferrals of as much as $19,500 in 2021, plus an additional $6,500 if you’re 50 or older, either on a pre-tax basis or as designated Roth contributions, which are made after payroll tax deductions and later generally distributed tax-free. You also are allowed to contribute as much as an additional 25% of your net earnings from self-employment for total contributions of $57,000 for 2021, including salary deferrals.

“To understand the contribution limits here, it helps to pretend you’re two people: An employer, of yourself, and an employee, also of yourself,” Kaminski says.

“In your capacity as the employee, you can contribute as you would to a standard employer-offered 401(k), with salary deferrals of up to 100% of your compensation or $19,500, whichever is less, plus that $6,500 catch-up contribution. In your capacity as the employer, you can make an additional contribution of up to 25% of compensation.”

The limit on compensation that can be used to factor your contribution is $285,000 in 2021. You also can choose a solo Roth 401(k), which mimics the tax treatment of a Roth IRA.

“You might go with this option if your income and tax rate are lower now than you expect them to be in retirement,” Kaminski says.

You can adapt your solo 401(k) to allow access to your account funds through loans and hardship distributions, but there can be restrictions and costly penalties. A solo 401(k) plan is generally required to file an annual report on IRS Form 5500-SF if it has $250,000 or more in assets at the end of the year, but a plan with a smaller balance may be exempt from the requirement.

Simplified Employee Pension (SEP) IRA. A SEP allows you to contribute as much as 25% of your net earnings from self-employment, not including contributions paid to yourself, as much as $57,000 for 2021. As with other types of retirement savings plans, the upper limit on contributions can increase from year to year. There is no provision for catch-up contributions.

SEPs function like traditional IRAs and 401(k)s in that distributions in retirement are taxed as income. There is no Roth version of a SEP.

A SEP allows for flexible annual contributions — you aren’t required to contribute every year — an advantage if cash flow could be an issue. However, loans from the account are not permitted, and the funds may not be used as collateral. In-service withdrawals are allowed, but the money counts as taxable annual income and is subject to a 10% additional tax if you are younger than 59 ½.

Establishing a SEP requires completion of a one-page form, either Form 5305-SEP (Simplified Employee Pension — Individual Retirement Accounts Contribution Agreement) from the IRS, which is available online, or an IRS-approved “prototype SEP plan” form offered by many mutual funds, banks and other financial institutions.

With the form completed, you can open a SEP-IRA through a bank or other financial institution. A SEP plan can be established as late as the due date of your income tax return for that year, including extensions. That means you could conceivably put thousands of dollars into a new SEP for a year already ended, providing a one-time opportunity to help you catch up on a late start on your retirement account.

Kaminski says the tax advantage of a SEP is that it allows you to deduct the lesser of your contributions or 25% of net self-employment earnings on your annual tax filing.

He says a SEP is best for self-employed people or small business owners with no or few employees. However, he warns that if you do have employees, a SEP requires you to contribute an equal percentage of salary for each eligible employee.

SIMPLE IRA. With a Savings Incentive Match Plan for Employees (SIMPLE) IRA, you are allowed to put all of your net earnings from self-employment in the plan, although the upper limit is $13,500 in 2021, plus an additional $3,000 if you’re 50 or older, plus a 2% fixed contribution. SIMPLE IRA contribution limits are significantly lower than those for a SEP IRA or solo 401(k), Kaminski notes, which could limit how much you can save for retirement.

Contributions are tax-deductible, but distributions in retirement are taxed.

To open a SIMPLE IRA plan, complete either IRS Form 5305-SIMPLE for use with a designated financial institution, Form 5304-SIMPLE not for use with a designated financial institution, or an IRS-approved “prototype SIMPLE IRA plan” offered by many mutual funds, banks and other financial institutions. With the form completed, you can establish a SIMPLE IRA through a bank or another financial institution.

A SIMPLE IRA can be established between Jan. 1 through Oct. 1. If you became self-employed after Oct. 1, you are allowed to open a SIMPLE IRA for the year as soon as “administratively feasible” after your business starts, according to IRS rules.

Kaminski says there is a 401(k) version of a SIMPLE, which works in much the same way but allows participants to take loans from their accounts, although this version requires more administrative oversight and can be more expensive to set up.

Also, funds may be withdrawn at any time from a SIMPLE IRA. However, unless you qualify for an exception, you will need to pay an additional 10% tax. This additional tax increases to 25% if you make the withdrawal within 2 years from when the plan is opened.

You won’t need to pay the additional tax on early withdrawals if you qualify for any of these exceptions:

- You’re 59 ½ or older.

- Your withdrawal is not more than:

- The unreimbursed medical expenses that exceed 10% of your adjusted gross income (7.5% if you or your spouse is 65 or older).

- The cost for your medical insurance while you’re unemployed.

- Your qualified higher education expenses.

- The withdrawal, as much as $10,000, is used to buy, build or rebuild a first home.

- Your withdrawal is taken as an annuity.

- Your withdrawal is a qualified military reservist distribution.

- You’re disabled.

- You’re the beneficiary of a deceased SIMPLE IRA owner.

- The withdrawal is the result of an IRS levy.

SIMPLE IRAs are available for self-employed farriers, but matching contributions requirements could make the plan expensive and impractical if there are additional employees, Kaminski says.

Select Advisor Group Inc. and its affiliates do not provide tax, legal or accounting advice. This article has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.